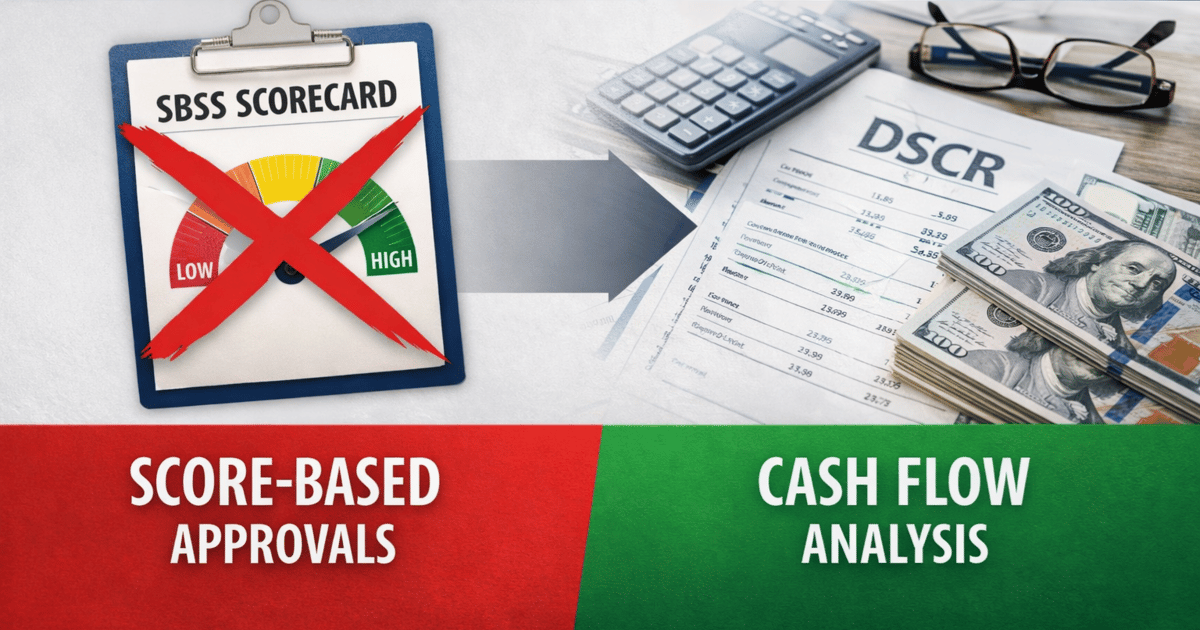

| | The End of Automated SBA Approvals | | | Beginning March 1, 2026, the SBA is discontinuing use of the FICO Small Business Scoring Service (SBSS) for 7(a) Small loans ($350,000 and under). | For years, the SBSS score wasn’t just an initial screen - in many high-volume SBA lending shops, it drove the credit decision. A traditional debt service coverage ratio was not calculated at all. The SBSS score was the primary indicator of repayment. | That gatekeeper is now gone. | Going forward, 7(a) Small loans ($350,000 and under) will require a calculated debt service coverage ratio, which will serve as the primary indicator of repayment instead of an automated SBA scorecard. | | | | | How Was the SBSS Score Previously Calculated? |

| No one really knows. The SBA never publicly disclosed the formula or weighting methodology. However, industry guidance and lender experience suggest the score generally incorporated a combination of the following: | Hard pull consumer credit report (owner/guarantor) Time in business/date of formation Public records, liens, or judgments Business credit data Other unknown factors

|

| |

| | |

| | | | | | My View From the Deal Desk |

| DSCR Is Back in Charge | Cash flow is cash flow. The approval decision now centers on whether the business can actually service the debt. This moves small loans closer to how large SBA loans ($350,001 - $5MM) have always been evaluated. | On larger transactions, no one asks what the score is - they ask whether the business can service the debt. The conversation shifts from “Did it clear the threshold?” to “Does it actually cash flow?” | Expect More Declines and Longer Wait Times | Automated screening accelerated volume and, in many cases, led to quicker approvals. When a score acted as the primary filter, decisions could be made quickly. If it cleared, the file advanced. If it didn’t, it stopped. Now, every 7(a) Small loan will require a documented DSCR calculation, supported by a business debt schedule. | Wiggle Room Continues to Shrink | As stated last week, flexibility within the program is tightening. As SOP guidance becomes more defined and more documented, judgment narrows. Deals that once moved forward on a score alone will now need measurable cash flow. Preparation and structure will directly influence outcomes. |

| |

| | |

| | | Cash flow now sits at the center of the decision for small loans, just as it has for larger ones. Small loans are no longer score-driven approvals. They are cash flow-driven credit decisions measured by DSCR. Expect slower processing and more back-and-forth with lenders. Outcomes will be less algorithmic and more grounded in hard data.

| | P.S. If you know a business owner, CPA, banker, broker, or attorney who might find this useful, feel free to pass it along. They can subscribe here. | | |

|